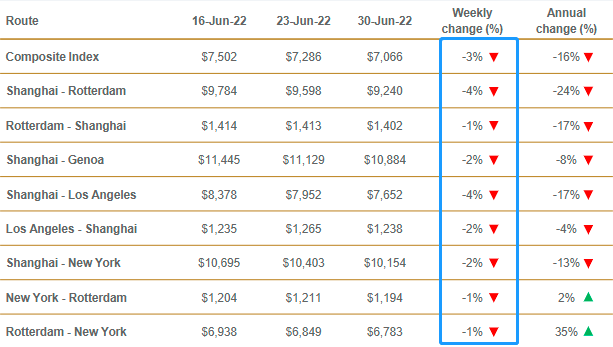

Recently, the British aviation consulting agency (Drewry) released the latest World Containerized Freight Index (WCI),which showed the WCI continued to fall 3% to $7,066.03/FEU. It is worth noting that the spot freight rate of the index, which is based on the eight major routes of Asia-America, Asia-Europe, and Europe and America, showed a comprehensive decline for the first time.

The WCI composite index fell 3% and was down 16% from the same period in 2021.Drewry’s year-to-date average WCI composite index is $8,421/FEU, however, the five-year average is only $3490/FEU, which is still $4930 higher.

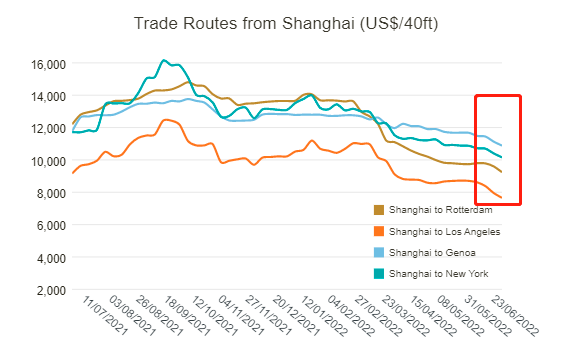

Spot freight from Shanghai to Los Angeles fell by 4% or $300 to $7,652/FEU. That’s down 16% from the same period in 2021.

Spot freight rates from Shanghai to New York fell 2% to $10,154/FEU.That’s down 13% from the same period in 2021.

Spot freight rates from Shanghai to Rotterdam fell by 4% or $358 to $9,240/FEU.That’s down 24% from the same period in 2021.

Spot freight rates from Shanghai to Genoa fell 2% to $10,884/FEU.That’s down 8% from the same period in 2021.

Los Angeles-Shanghai, Rotterdam-Shanghai, New York-Rotterdam and Rotterdam-New York spot rates all declined 1%-2% .

Drewry expects freight rates would continue to fall in the coming weeks.

Some industry investment consultants said that the super cycle of shipping has ended, and the freight rate will decline rapidly in the second half of the year.According to its estimation,The growth of global container shipping demand would decelerate from 7% in 2021 to 4% and 3% in 2022-2023,the third quarter would be a turning point。

From the perspective of the overall supply and demand relationship, the supply bottleneck has been opened, and the loss of transportation efficiency will no longer be lost. The vessel loading capacity increased 5% in 2021, efficiency lost 26% due to port plugging,which pull down real supply growth to only 4%,but during 2022-2023,with the widespread vaccination of the covid-19,since the first quarter, the knock-on effect of the original restrictions on port loading and unloading has been significantly alleviated, Gradual resumption of truck and intermodal operations, the acceleration of container flow, the reduction of the quarantine amount of dock workers and the lifting of slack, and the increase in the speed of ships, etc.

The third quarter is the traditional peak season for shipping. According to industry insiders, according to the usual practice, European and American retailers and manufacturing companies began to pull goods in July.I am afraid that the price trend will be clearer until mid-to-late July.

In addition, according to last week’s data released by Shanghai Shipping Exchange, the Shanghai Export Containerized Freight Index (SCFI) index fell for two consecutive weeks, down 5.83 points, or 0.13%, to 4216.13 points last week.The freight rates of the three major ocean routes continued to be revised, of which the eastern route of the United States fell by 2.67%, which was the first time that it fell below the US$10,000 since the end of July last year.

Analysts believe that the current market is full of variables. Factors such as the Russian-Ukrainian conflict, global strikes, interest rate hikes by the Federal Reserve, and inflation may curb European and American demand. In addition, the cost of raw materials, transportation and logistics is high, and foreign trade manufacturers tend to be conservative in preparing materials and production.At the same time, the number of ships in the port of Messiah decreased, the supply of transportation capacity increased, and the freight rate continued to adjust at a high level.

Post time: Jul-14-2022